Stock markets specialized in smaller businesses are, of course, nothing new. As early as the 1970s, there were trading platforms tailored to the needs and capabilities of SMEs. However, their true evolution only came in the 1990s. These markets are known as “junior” or “feeder” markets, since they were set up predominantly as segments of the main markets of national stock exchanges and their role was to “feed in” issuers for the main market. Although the dot-com bubble and the financial crisis also halted the development of minor markets, the importance of SME markets is increasingly recognized by the EU. Consequently, “SME growth markets” are expected to play a significant role in the European Commission’s Capital Markets Union package. In our article, we will present the key SME markets and players, and also the development and rules of such markets.

Issuers and investors on the SME market

The universal functions of the stock exchange also apply to a market specialized in SMEs. In the case of a new issuance (of shares), i.e. on the “primary” market, the stock market’s capital allocation role is the most important one, which means that the exchange is one of the channels for financial intermediation between investors and issuers. When already-issued securities are traded (the “secondary” market), the liquidity function of the market is more pronounced: it becomes an institution that helps implement the purchase and sale transactions of securities. Additionally, for both the primary and the secondary markets, the stock exchange provides the price discovery function and makes available information influencing prices within a standardised framework. The same primary and secondary market functions are also predominant in the case of an SME market. However, issuers and investors have slightly different perspectives compared to the main markets that trade in the stock of large enterprises.

Companies listing on SME markets want to exploit the benefits of listing and they strive to lay the foundation for main-market transactions. Although smaller companies mostly choose loans when they require new financial resources, a number of businesses, typically focusing on services and growing rapidly, cannot provide the material collateral necessary for an investment loan. If a small or medium-sized enterprise wants to grow, it needs to gradually increase its capital. Because other forms of raising capital (e.g. venture capital) are not suitable to cover the entire range of SME types, the stock exchange can be the most appropriate form of acquiring long-term financing for some SMEs, more likely supplementing, but not replacing, loans and/or private financing sources. It is an important consideration (and at times it is the most important) that the reputation value of stock market presence can also be exploited, which strengthens the visibility of the issuers and their brand value. This could potentially improve the business and the financial figures of a company. It is also a motivating factor for issuer SMEs that they want to enter the main market with time, and they establish their public operation on the junior markets for this reason.

From the junior to the main market

The Mears Group, a British company, is a typical example of how significant growth can be achieved through capital market financing and how an SME can become a dominant market player and a large company through the exchange. When this company offering maintenance and renovation services to households and commercial outlets choose listing in 1996, it managed to generate a turnover of GBP 12 million, although the company only employed a total of 83 people. The company’s shares were listed first on AIM, the London SME market. Its capitalisation at the time amounted to GBP 3.6 million. Three years later, taking advantage of its business success and a wide range of financing options, Mears carried out its first major acquisition. It purchased Haydon & Co, a company with 500 employees. By 2008, Mears had 8,000 employees and was valued at GBP 213.5 million. It also entered the main market of the London Stock Exchange. Today, following a period of strong organic growth and a number of successful acquisitions, the Mears Group has over 15,000 employees and its sale revenue exceeds GBP 800 million.

However, SMEs can have a hard time when they have to meet the stringent requirements of regulated markets. The regulation of main markets requires a wide range and considerable depth of information from issuers. The disclosure obligation covers business, financial and practically all other categories of information that may impact shareholder value. It is a time-consuming and expensive process to collect and organise such data, which results in significant preparatory and other costs for basically all companies. Although the costs vary, to a large extent depending on the characteristics of the market, the company and the transaction, the first public transaction generally requires one year of preparation and a cost burden of 5 to 15% for issuers in proportion to the total capital raised. This figure includes the official licence fees as well as the less direct preparation costs (investment service provider, legal services, adopting to accounting standards, marketing expenses, etc.). Since SMEs are typically in the early stages of the company development curve both in terms of financial indicators and organisational development, the above cost burden may be greater and the time required for preparation may be longer in the case of implementing a public transaction. For this reason, SME markets typically set less stringent criteria that better match the level that SMEs can match. We will describe this phenomenon below in more detail.

SME markets can serve as an appropriate platform for both traditional and new players investing in SMEs. The SME bankruptcy rate is higher and, even if bankruptcies are avoided, the business performance of SMEs tends to fluctuate more than that of large enterprises. SME shares also generally have low liquidity. For this reason – it is worth immediately pointing out – SME shares are riskier than large enterprise equity, which means that they attract investors with a higher level of risk appetite. Among small investors, this asset class is held for diversification purposes by more affluent households, which have a better risk-taking ability. Beyond them, institutional investors (which can be best compared to risk-capital ventures) that think long-term own a substantial share in listed SMEs. They are the ones that usually organise the capital-raising process and the listing as lead investors. (Later, we will discuss that capital is very rarely raised directly through the stock exchange, but the presence in itself increases the chances both for raising capital successfully and for higher pricing, due to its reputation effect and the fact that it is publicly listed.) Also, in the most liquid SME markets, the traditional representatives of institutional investors (i.e. pension funds and insurance companies) also appear, and they typically acquire SME exposure for diversification purposes.

The operation of the SME market

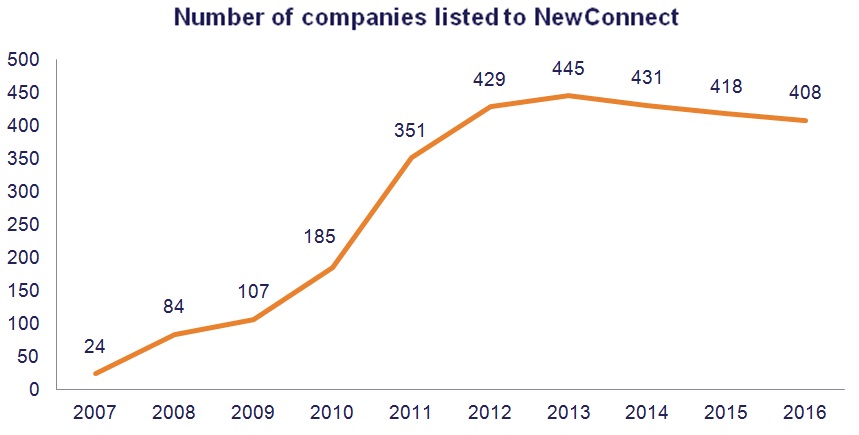

Operators of markets focusing on SMEs make an important distinction between the junior section and the regulated market. The distinction materializes in different forms: in a branding separate from the main market’s, in unique market players and individual investment protection mechanisms aimed at counter-balancing the lax regulatory environment, in lower fees and in easier listing criteria. The most successful European SME markets include AIM, which is operated by the London Stock Exchange, and Nasdaq First North, which is held by the Nordic subsidiary of the US stock exchange in our region, NewConnect, which was founded in 2007 by the Warsaw stock exchange, has shown substantial growth (see fig. 2). These markets were built on the same pillars and followed the strategy that made capital market financing a viable option for SMEs.

Source: NewConnect – Annual market statistics, September 2016

Source: NewConnect – Annual market statistics, September 2016

The key to operation satisfying both the company’s and the investors’ interests is striking a balance between a market-friendly environment and investment protection. SME markets typically operate as MTFs. One of the key characteristics of MTFs is that a number of regulatory functions are transferred from the local supervisory authority to the operator of the market (in this case, the stock exchange). Stock exchanges can be flexible when assessing individual listing applications, and the administrative burden is smaller for companies. Furthermore, the costs of listing and continuous presence in the stock exchange are to a large extent lessened for issuers when compared to the fees of a regulated market. In order to ensure that the interests of investors are upheld to the extent possible, despite the supervisory authority taking a back seat, stock exchanges typically require issuers to use the services of a group of intermediaries, the so-called nominated advisors.

Nominated advisors have a dual role. On the one hand, they help the enterprise’s preparation from the very beginning of the listing procedure, but on the other hand, they offer a guarantee to the investors that the issuers at the SME market are of high quality and well-prepared. Nominated advisor licences are handed out by the stock exchange to market players. The companies must hire one of them before listing. The nominated advisor assesses whether the company is ready for the stock market and, in cooperation with external consultants and the company itself, the nominated advisor compiles the listing documentation. It is a key role of the nominated advisor (and this separates them from the consultants that support listing on the main market) that they continue to support the company after listing in connection with operation in compliance with market rules and, if they identify shortcomings, they are required to report them to the operator of the market.

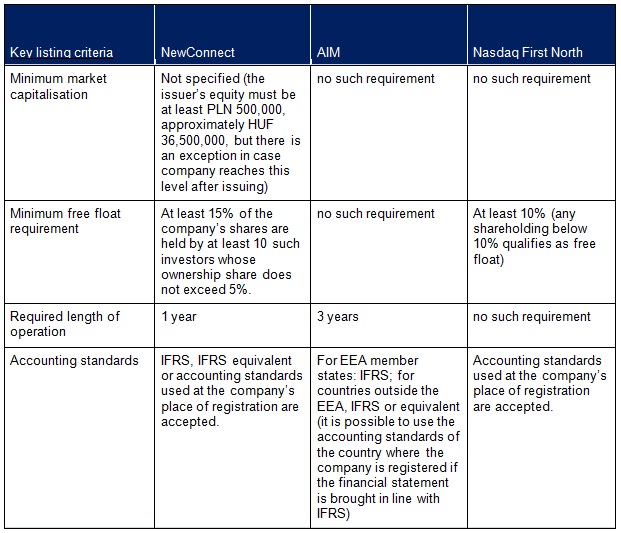

The listing criteria in the SME markets are tailored to smaller-sized companies. Stock exchanges generally have significantly less stringent requirements for SMEs as compared to the main market. The following listing criteria apply in the Polish, British and Nordic cases mentioned above:

Listing criteria for SME markets

The method of raising capital is different from the more traditional IPOs typically used for new listings. The Prospectus Directive of the EU requires companies raising capital to prepare a prospectus in the case of a public offering exceeding EUR 5 million, and they must have it approved by the relevant supervisory authorities. This quantitative restriction can be overcome if companies issue shares through private placement and then list them on the SME market without public offering. Later, retail investors can join. Private placement makes it possible to limit the primary subscription to securities to a maximum number of 149 private investors or an unlimited number of qualified investors.

It can also be achieved in Hungary

It is an integral part of the BSE’s 5-year strategy to increase the number of issuers and to make the advantages of raising capital through and operating at the stock exchange accessible to as many enterprises as possible. A key element of this goal is to develop an SME market in Hungary that, based on international examples, can be an important platform for funding high-growth companies and a breeding ground for them to become large enterprises.

On the basis of international examples and our own experience, a substantial issuer base and interest can be identified among SMEs. Smaller listed companies and the supervisory authority concluded that there are quite a few, typically smaller, companies for which a regulated market means too many constraints and too-high costs. For them, a market with less stringent publication rules would likely be more acceptable. The BSE’s experience so far shows that a number of credible company leaders as well as ambitious companies with stable or increasing growth can be identified whose investment “story” might interest the stock market. In a scoring exercise, we found 300 companies mature enough for the stock market. We published with Figyelő and KPMG a list of 50 enterprises with high potential and met with the representatives of nearly 70 businesses in person over the past six months. In order to make this story as complete and attractive as possible, the BSE launched a corporate finance programme in cooperation with London Stock Exchange’s ELITE initiative to target owners and managers of companies that are in a rapid growth phase and might consider the use of external financing.

The investor and advisory infrastructures are ready to enter the SME market. The players in the risk capital industry, which has been on the rise in Hungary over the past 5 to 10 years, should take the SME market into account as investors, as salespersons, and also at times when they look for co-investors. Moreover, because of the current low-yield environment, domestic private investors open to riskier investments might find an opportunity in Hungary, too. The existing consulting firms provide an excellent foundation for the development of the market by making available the required pool of nominated advisors.

Building a market, of course, is difficult: new structures need to be developed for both the investors and the issuers. Furthermore, investment protection and other considerations need to be balanced carefully when the rules are adopted. It is our hope that the new year will bring not only a start for adopting the system of rules, but also the development of the advisors’ ecosystem and new listings.